1 The Company

Wesdome Gold Mines (WDOFF) exlores for, mines, and develops mineral resource properties, primarily gold in Canada.

| Number of shares (May 1, 2014) | 111,107,591 |

| Number of options (May 1, 2014) | 3,328,116 |

| Convertible debentures (May 1, 2014) | 2,808,400 |

| Fully diluted number of shares (May 1, 2014) | 117,244,107 |

| Share price | $0.84 |

| Market cap | $93.3 million |

| Ticker | TSX:WDO,WDOFF |

1.1 History

Wesdome Gold Mines was founded in 1976 and became a publicly listed company in 1999. Wesdome merged with River Gold Mines in February 2006 and again with Western Quebec Mines in July 2007. The company has produced over 1.3 million ounces of gold over the last 25 years.

(Source: Wesdome)

1.2 Business Model

Wesdome is 100% unhedged to gold price and has never hedged. The company's strengths are quality gold deposits and an experienced, efficient operating team. Wesdome is a low-overhead, no-nonsense, owner-operated company working for its shareholders.

1.3 Mines

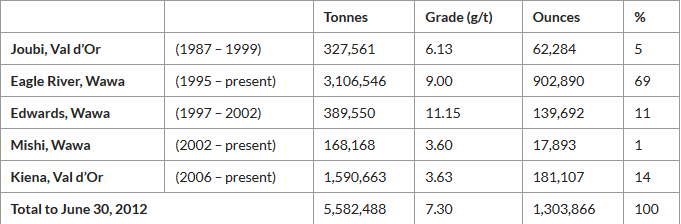

Wesdome has two producing mines located in Canada.

(Source: Investor presentation)

Eagle River Mine

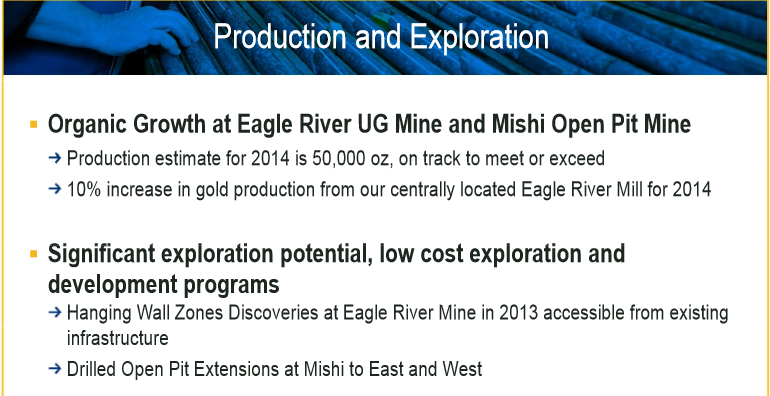

The Eagle River mine is located 50 kilometers due west of Wawa, Ontario, and 60 kilometers southeast of Hemlo. The Eagle River property was purchased in 1994 and the first gold bar was poured in October 1995. The Eagle River mine has produced more than 950,000 ounces since 1995 at an average grade of 9.1 g/tonne. In 2013, Eagle River produced 42,850 gold ounces. The production has grown 52% since 2011.

| Year | 2011 | 2012 | 2013 |

| Production (ounces) | 28,200 | 32,200 | 42,850 |

The 2014 production forecast is 44,000 gold ounces.

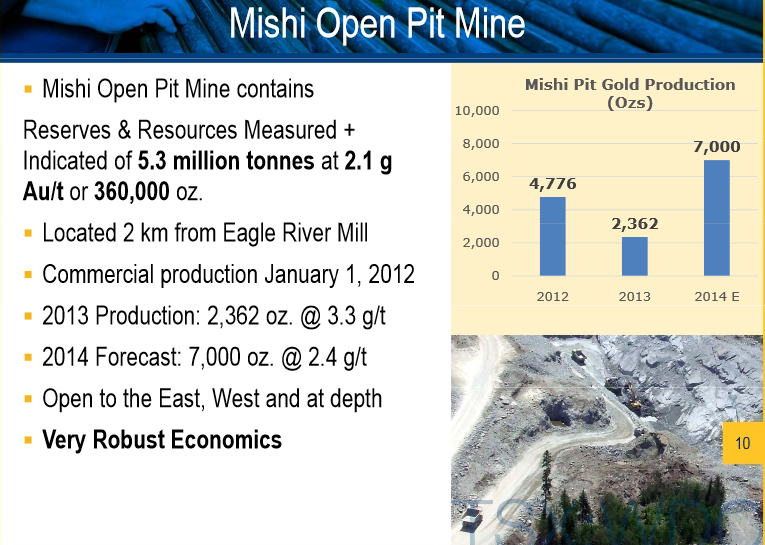

Mishi Mine

The Mishi mine is situated 15 kilometers north of the Eagle River mine and 2 kilometers from the Eagle River mill. Commercial production at Mishi mine started in January 2012. The production is expected to reach 7,000 ounces this year.

(Source: Investor presentation)

Gold reserves at the Eagle River complex have grown 285% since 2008.

(Source: Investor presentation)

2 Management

Rowland Uloth has been the CEO since August 2013. Collectively, Wesdome's executive team has over 70 years of industry experience.

(Source: Investor presentation)

2.1 Insider Ownership

Wesdome's directors and executive officers own 2% of the company.

Here is a table of Wesdome's insider activity by calendar month.

| | Insider buying / shares | Insider selling / shares |

| July 2014 | 0 | 0 |

| June 2014 | 0 | 0 |

| May 2014 | 0 | 0 |

| April 2014 | 5,194 | 0 |

| March 2014 | 24,500 | 0 |

| February 2014 | 10,000 | 0 |

| January 2014 | 0 | 0 |

| December 2013 | 50,000 | 0 |

| November 2013 | 50,000 | 0 |

| October 2013 | 50,000 | 0 |

| September 2013 | 100,000 | 0 |

| August 2013 | 42,800 | 0 |

| July 2013 | 0 | 0 |

| June 2013 | 30,000 | 0 |

| May 2013 | 0 | 0 |

| April 2013 | 27,000 | 0 |

| March 2013 | 5,000 | 0 |

| February 2013 | 0 | 0 |

| January 2013 | 150,000 | 0 |

(Note: The table does not include shares purchased by Wesdome. Wesdome has purchased 135,700 shares during April 2013 to July 2014 time period.)

There have been 544,494 shares purchased and there have been zero shares sold by insiders since January 2013.

2.2 Compensation

Here is a table of Wesdome's executive compensation.

(Source: Annual shareholders meeting)

None of the executive officers were paid base salaries more than $200,000 in 2013.

3 Operating Summary

Here is a table of Wesdome's annual gold production since 2008.

| Year | Annual production (ounces) |

| 2008 | 90,004 |

| 2009 | 96,152 |

| 2010 | 68,874 |

| 2011 | 47,747 |

| 2012 | 55,813 |

| 2013 | 52,980 |

The gold production peaked in 2009.

4 Financial Summary

4.1 Current Situation

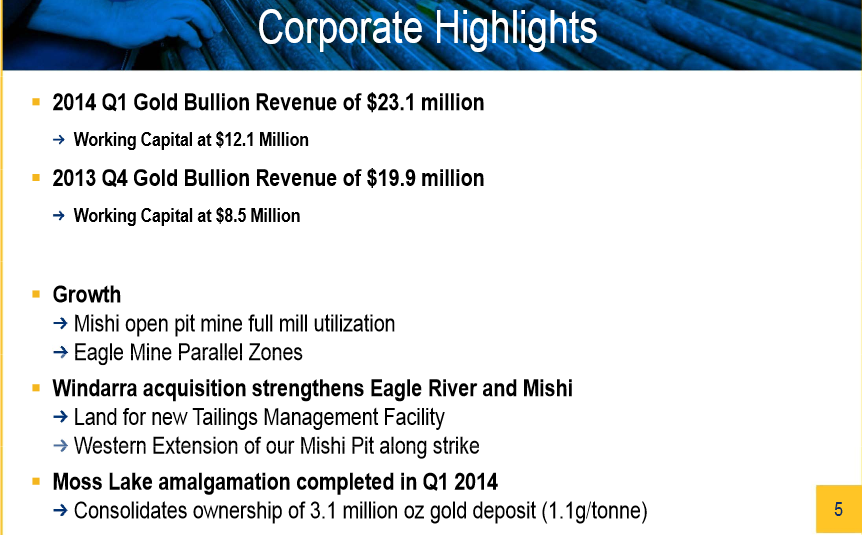

Wesdome reported the first-quarter financial results on May 1 with the following highlights:

| Revenue | C$23.1 million |

| Net income | C$4.2 million |

| Cash | C$7.9 million |

| Debt | C$7.7 million |

| Gold production | 13,730 ounces |

| Production cost | C$977 per ounce |

(Source: Investor presentation)

4.2 Historical Developments

Here is a table of Wesdome's revenue and earnings since 2008.

| Year | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 |

| Revenue (C$ millions) | 80.3 | 103.5 | 89.4 | 79.6 | 92.3 | 79.7 |

| Net income/loss (C$ millions) | 9.4 | 32.2 | 5.3 | 0.2 | -45.3 | -3.9 |

| EPS | 0.09 | 0.32 | 0.05 | 0.00 | -0.44 | -0.04 |

Wesdome's revenue and earnings peaked in 2009.

5 Shares

Here is a table of Wesdome's number of shares since 2008.

| Year | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 |

| Number of shares (millions) | 99.8 | 100.1 | 100.8 | 101.7 | 101.9 | 102.9 |

Wesdome's number of shares have grown only 3.1% since 2008.

6 Outlook

Wesdome's 2014 production guidance is 50,000 gold ounces.

(Source: Investor presentation)

Wesdome's global gold resources are 5.1 million ounces.

(Source: Investor presentation)

7 Risks

I believe the two main risks are the gold price and relatively low gold reserves. Wesdome's production costs were C$977 per ounce in the first quarter. The company's current gold reserves in the Eagle River complex are 281,000 ounces, which will last for about five years. Wesdome is also a penny stock.

8 Conclusion

Wesdome's Eagle River mine has produced more than 950,000 ounces since 1995 at a very high grade of 9.1 g/tonne. The company's production costs were below $1,000 per ounce in the most recent quarter. Wesdome's gold resources are currently 5.1 million ounces, which gives the company ample room to grow. The insiders have been buying the stock since 2013. I believe Wesdome could be a good pick below $1 based on the insider buying.

(Source: Investor presentation)

Disclosure: The author is long TSX:WDO

About the author:maarnioI have 15 years of investing experience. I have traded stocks, commodities and Forex markets.

| Currently 0.00/512345 Rating: 0.0/5 (0 votes) | |

Subscribe via Email

Subscribe RSS Comments Please leave your comment:

More GuruFocus Links

| Latest Guru Picks | Value Strategies |

| Warren Buffett Portfolio | Ben Graham Net-Net |

| Real Time Picks | Buffett-Munger Screener |

| Aggregated Portfolio | Undervalued Predictable |

| ETFs, Options | Low P/S Companies |

| Insider Trends | 10-Year Financials |

| 52-Week Lows | Interactive Charts |

| Model Portfolios | DCF Calculator |

RSS Feed  | Monthly Newsletters |

| The All-In-One Screener | Portfolio Tracking Tool |

MORE GURUFOCUS LINKS

| Latest Guru Picks | Value Strategies |

| Warren Buffett Portfolio | Ben Graham Net-Net |

| Real Time Picks | Buffett-Munger Screener |

| Aggregated Portfolio | Undervalued Predictable |

| ETFs, Options | Low P/S Companies |

| Insider Trends | 10-Year Financials |

| 52-Week Lows | Interactive Charts |

| Model Portfolios | DCF Calculator |

| RSS Feed | Monthly Newsletters |

| The All-In-One Screener | Portfolio Tracking Tool |

TSX:WDO STOCK PRICE CHART

0.88 (1y: +144%) $(function(){var seriesOptions=[],yAxisOptions=[],name='TSX:WDO',display='';Highcharts.setOptions({global:{useUTC:true}});var d=new Date();$current_day=d.getDay();if($current_day==5||$current_day==0||$current_day==6){day=4;}else{day=7;} seriesOptions[0]={id:name,animation:false,color:'#4572A7',lineWidth:1,name:name.toUpperCase()+' stock price',threshold:null,data:[[1374469200000,0.36],[1374555600000,0.365],[1374642000000,0.38],[1374728400000,0.41],[1374814800000,0.385],[1375074000000,0.4],[1375160400000,0.42],[1375246800000,0.395],[1375333200000,0.408],[1375765200000,0.395],[1375851600000,0.398],[1375938000000,0.4],[1376024400000,0.405],[1376283600000,0.38],[1376370000000,0.41],[1376456400000,0.38],[1376542800000,0.4],[1376629200000,0.395],[1376888400000,0.4],[1376974800000,0.485],[1377061200000,0.55],[1377147600000,0.65],[1377234000000,0.69],[1377493200000,0.7],[1377579600000,0.73],[1377666000000,0.67],[1377752400000,0.65],[1377838800000,0.64],[1378184400000,0.7],[1378270800000,0.68],[1378357200000,0.66],[1378443600000,0.69],[1378702800000,0.7],[1378789200000,0.67],[1378875600000,0.64],[1378962000000,0.64],[1379048400000,0.64],[1379307600000,0.63],[1379394000000,0.55],[1379480400000,0.73],[1379566800000,0.7],[1379653200000,0.66],[1379912400000,0.62],[1379998800000,0.65],[1380085200000,0.67],[1380171600000,0.69],[1380258000000,0.69],[1380517200000,0.7],[1380603600000,0.64],[1380690000000,0.61],[1380776400000,0.61],[1380862800000,0.56],[1381122000000,0.59],[1381208400000,0.66],[1381294800000,0.61],[1381381200000,0.6],[1381467600000,0.58],[1381813200000,0.56],[1381899600000,0.57],[1381986000000,0.56],[1382072400000,0.56],[1382331600000,0.59],[1382418000000,0.65],[1382504400000,0.62],[1382590800000,0.63],[1382677200000,0.66],[1382936400000,0.68],[1383022800000,0.71],[1383109200000,0.7],[1383195600000,0.66],[1383282000000,0.66],[1383544800000,0.66],[1383631200000,0.64],[1383717600000,0.68],[1383804000000,0.64],[1383890400000,0.66],[1384149600000,0.6],[1384236000000,0.57],[1384322400000,0.52],[1384408800000,0.56],[1384495200000,0.55],[1384754400000,0.51],[1384840800000,0.58],[1384927200000,0.55],[1385013600000,0.57],[1385100000000,0.55],[1385359200000,0.59],[1385445600000,0.57],[1385532000000,0.58],[1385618400000,0.62],[1385964000000,0.56],[! 1386050400000,0.58],[1386136800000,0.61],[1386223200000,0.58],[1386309600000,0.58],[1386568800000,0.58],[1386655200000,0.6],[1386741600000,0.57],[1386828000000,0.6],[1386914400000,0.58],[1387173600000,0.65],[1387260000000,0.63],[1387346400000,0.63],[1387432800000,0.62],[1387519200000,0.58],[1387778400000,0.56],[1387864800000,0.57],[1388124000000,0.63],[1388383200000,0.6],[1388469600000,0.58],[1388642400000,0.63],[1388728800000,0.63],[1388988000000,0.61],[1389074400000,0.64],[1389160800000,0.59],[1389247200000,0.61],[1389333600000,0.62],[1389592800000,0.63],[1389679200000,0.63],[1389765600000,0.65],[1389852000000,0.66],[1389938400000,0.68],[1390197600000,0.68],[1390284000000,0.73],[1390370400000,0.75],[1390456800000,0.74],[1390543200000,0.75],[1390802400000,0.68],[1390888800000,0.68],[1390975200000,0.7],[1391061600000,0.72],[1391148000000,0.67],[1391407200000,0.69],[1391493600000,0.69],[1391580000000,0.68],[1391666400000,0.68],[1391752800000,0.7],[1392012000000,0.72],[1392098400000,0.78],[1392184800000,0.74],[1392271200000,0.77],[1392357600000,0.8],[1392703200000,0.83],[1392789600000,0.8],[1392876000000,0.82],[1392962400000,0.83],[1393221600000,0.79],[1393308000000,0.76],[1393394400000,0.8],[1393480800000,0.84],[1393567200000,0.79],[1393826400000,0.95],[1393912800000,0.9],[1393999200000,0.91],[1394085600000,0.93],[1394172000000,0.91],[1394427600000,0.92],[1394514000000,0.92],[1394600400000,0.94],[1394686800000,0.94],[1394773200000,0.95],[1395032400000,0.94],[1395118800000,0.9],[1395205200000,0.8],[1395291600000,0.85],[1395378000000,0.82],[1395637200000,0.8],[1395723600000,0.74],[1395810000000,0.75],[1395896400000,0.74],[1395982800000,0.78],[1396242000000,0.73],[1396328400000,0.72],[1396414800000,0.77],[1396501200000,0.77],[1396587600000,0.8],[1396846800000,0.79],[1396933200000,0.82],[1397019600000,0.79],[1397106000000,0.78],[1397192400000,0.79],[1397451600000,0.8],[1397538000000,0.76],[1397624400000,0.76],[1397710800000,0.76],[1398056400000,0.76],[1398142800000,0.77],[1398229200000,0.77],[1398

Food prices have been rising, but don't fear: Not all groceries are more expensive. All the fixings for peanut butter and jelly are cheaper now than they were a year ago. NEW YORK (CNNMoney) It's peanut butter jelly time.

Food prices have been rising, but don't fear: Not all groceries are more expensive. All the fixings for peanut butter and jelly are cheaper now than they were a year ago. NEW YORK (CNNMoney) It's peanut butter jelly time.  Andrew Harrer/Bloomberg via Getty Images BERLIN and MILAN -- Fiat Chrysler has denied a magazine report saying it's in merger talks with Volkswagen, while the German carmaker said it had no takeovers on its agenda. Germany's Manager Magazin said Thursday Volkswagen Chairman Ferdinand Piech had held talks with the owners of Fiat Chrysler about buying all or part of the group that was formed this year from the merger of Italian and U.S. carmakers. The magazine cited unnamed company sources. However, a VW spokesman said Europe's biggest carmaker was focused on delivering improvements at its existing operations. "There are currently no [merger and acquisition] projects on the agenda," he said. "We are now focusing on boosting efficiency across the group." The Agnelli family's holding firm Exor, which owns a 30 percent stake in Fiat Chrysler, denied any talks had taken place, as did Fiat Chrysler. Shares in Fiat Chrysler jumped 5 percent to 7.98 euros on the report, but had retreated to stand up 2.2 percent by 1352 GMT (9:52 a.m. Eastern time). VW's stock was 1.8 percent lower. VW Chief Executive Officer Martin Winterkorn said in March the carmaker, though hoarding almost 18 billion euros ($24 billion) in cash, had no plans to expand the group through acquisitions as it was focusing on integrating its 12 brand network. VW has since sealed a 6.7 billion euro buyout of minority shareholders at Swedish truck division Scania to forge a long-planned alliance of its truck brands. The report could suggest "diverging views" between VW's management and the supervisory board about the carmaker's future course, said Arndt Ellinghorst, a London-based analyst at investment researchers ISI Group, at a time when Winterkorn, 67, and Piech, 77, are soon likely to face a debate over succession. Rather than talking about further expansion, top managers at VW -- concerned that profitability gains aren't keeping pace with the company's steadily growing size -- have been pushing a new efficiency program that includes 5 billion euros of cost cuts per year at the core passenger car brand. Earlier this month, VW also denied a report it was planning a bid for U.S. truck maker Paccar next year. Interested In Assets "The risks from integrating Italian plants and managing a U.S. business are material and we do not believe that the potential benefits justify the risks," Ellinghorst wrote in a note to clients. A person familiar with the situation told Reuters that VW would more likely bid for Fiat assets such as Magnetti or Alfa Romeo rather than the entire company. A member of VW's supervisory board, which oversees the management board, said the 20 member panel had at no point of time had any discussions about a purchase of Fiat. Still, Piech and Winterkorn have repeatedly expressed interest in Alfa Romeo despite rebuttals from Fiat CEO Sergio Marchionne. Manager Magazin said VW was hoping to use Chrysler's U.S. distribution network to help solve its own problems in the world's No. 2 auto market where flagging sales of the VW brand in January sparked the ouster of VW's regional chief. However, VW's U.S. troubles "are more image and pricing problems and not so much problems of distribution and manufacturing," an auto analyst said. "Buying Chrysler would not really help VW." Fiat took full control of Chrysler at the start of 2014, creating the world's No. 7 auto group, and plans to list the merged Fiat Chrysler Automobiles in New York later this year. Chief Executive Officer Sergio Marchionne has said he wants Fiat Chrysler to follow bigger rivals such as VW by building global brands and strengthening its position in the fast-growing and high-margin market for premium cars. The company is counting on its founding merger and a U.S. listing to help foot the bill for its 48 billion euro plan to grow net profit fivefold and sales by 60 percent by 2018. While rumors of a potential Agnelli family exit have surfaced over the years in Italian press, Exor has repeatedly said the stake remained a strategic investment for the family. Manager Magazin also said VW and Fiat Chrysler's owners were far from reaching an agreement about a possible price. -. MSRP: $26,495 Resale value retained after five years: 50.5 percent Even under Fiat (FIATY) ownership, some elements of Dodge's mouth-breathing, knuckle-dragging, He-Man-Woman-Haters-Club approach to auto sales managed to survive. The built-by-car-guys-for-car-guys Challenger and its rebooted muscle car aesthetic still lingers to lure meatheads who value racing stripes and rims over, oh, just about any other element of their vehicle. Ordinarily, that alone wouldn't make one of these vehicles worth a second look five years from now -- even among the most superficial gearheads. But Fiat helped the Challenger smarten up a little bit by coupling a 305-horsepower V6 engine or 375-horsepower 5.7-liter V8 Hemi with loads of interior space, real-time touchscreen navigation, traffic updates, Bluetooth connectivity, Sirius (SIRI) XM satellite radio, keyless entry/starter and a whole lot of Harman Kardon audio upgrades.

Andrew Harrer/Bloomberg via Getty Images BERLIN and MILAN -- Fiat Chrysler has denied a magazine report saying it's in merger talks with Volkswagen, while the German carmaker said it had no takeovers on its agenda. Germany's Manager Magazin said Thursday Volkswagen Chairman Ferdinand Piech had held talks with the owners of Fiat Chrysler about buying all or part of the group that was formed this year from the merger of Italian and U.S. carmakers. The magazine cited unnamed company sources. However, a VW spokesman said Europe's biggest carmaker was focused on delivering improvements at its existing operations. "There are currently no [merger and acquisition] projects on the agenda," he said. "We are now focusing on boosting efficiency across the group." The Agnelli family's holding firm Exor, which owns a 30 percent stake in Fiat Chrysler, denied any talks had taken place, as did Fiat Chrysler. Shares in Fiat Chrysler jumped 5 percent to 7.98 euros on the report, but had retreated to stand up 2.2 percent by 1352 GMT (9:52 a.m. Eastern time). VW's stock was 1.8 percent lower. VW Chief Executive Officer Martin Winterkorn said in March the carmaker, though hoarding almost 18 billion euros ($24 billion) in cash, had no plans to expand the group through acquisitions as it was focusing on integrating its 12 brand network. VW has since sealed a 6.7 billion euro buyout of minority shareholders at Swedish truck division Scania to forge a long-planned alliance of its truck brands. The report could suggest "diverging views" between VW's management and the supervisory board about the carmaker's future course, said Arndt Ellinghorst, a London-based analyst at investment researchers ISI Group, at a time when Winterkorn, 67, and Piech, 77, are soon likely to face a debate over succession. Rather than talking about further expansion, top managers at VW -- concerned that profitability gains aren't keeping pace with the company's steadily growing size -- have been pushing a new efficiency program that includes 5 billion euros of cost cuts per year at the core passenger car brand. Earlier this month, VW also denied a report it was planning a bid for U.S. truck maker Paccar next year. Interested In Assets "The risks from integrating Italian plants and managing a U.S. business are material and we do not believe that the potential benefits justify the risks," Ellinghorst wrote in a note to clients. A person familiar with the situation told Reuters that VW would more likely bid for Fiat assets such as Magnetti or Alfa Romeo rather than the entire company. A member of VW's supervisory board, which oversees the management board, said the 20 member panel had at no point of time had any discussions about a purchase of Fiat. Still, Piech and Winterkorn have repeatedly expressed interest in Alfa Romeo despite rebuttals from Fiat CEO Sergio Marchionne. Manager Magazin said VW was hoping to use Chrysler's U.S. distribution network to help solve its own problems in the world's No. 2 auto market where flagging sales of the VW brand in January sparked the ouster of VW's regional chief. However, VW's U.S. troubles "are more image and pricing problems and not so much problems of distribution and manufacturing," an auto analyst said. "Buying Chrysler would not really help VW." Fiat took full control of Chrysler at the start of 2014, creating the world's No. 7 auto group, and plans to list the merged Fiat Chrysler Automobiles in New York later this year. Chief Executive Officer Sergio Marchionne has said he wants Fiat Chrysler to follow bigger rivals such as VW by building global brands and strengthening its position in the fast-growing and high-margin market for premium cars. The company is counting on its founding merger and a U.S. listing to help foot the bill for its 48 billion euro plan to grow net profit fivefold and sales by 60 percent by 2018. While rumors of a potential Agnelli family exit have surfaced over the years in Italian press, Exor has repeatedly said the stake remained a strategic investment for the family. Manager Magazin also said VW and Fiat Chrysler's owners were far from reaching an agreement about a possible price. -. MSRP: $26,495 Resale value retained after five years: 50.5 percent Even under Fiat (FIATY) ownership, some elements of Dodge's mouth-breathing, knuckle-dragging, He-Man-Woman-Haters-Club approach to auto sales managed to survive. The built-by-car-guys-for-car-guys Challenger and its rebooted muscle car aesthetic still lingers to lure meatheads who value racing stripes and rims over, oh, just about any other element of their vehicle. Ordinarily, that alone wouldn't make one of these vehicles worth a second look five years from now -- even among the most superficial gearheads. But Fiat helped the Challenger smarten up a little bit by coupling a 305-horsepower V6 engine or 375-horsepower 5.7-liter V8 Hemi with loads of interior space, real-time touchscreen navigation, traffic updates, Bluetooth connectivity, Sirius (SIRI) XM satellite radio, keyless entry/starter and a whole lot of Harman Kardon audio upgrades.

Rumors like this often come from sketchy sources in AAPL's Asian supply chain, but in this case we actually have video evidence, one from blogger Marques Brownlee and another made in China.

Rumors like this often come from sketchy sources in AAPL's Asian supply chain, but in this case we actually have video evidence, one from blogger Marques Brownlee and another made in China.  One chart was developed by research firm Gartner, Inc., and is known as the Gartner Hype Cycle. It's intended as a tool to help investors and business executives assess where an emerging technology stands so they can determine when the time is right to jump in.

One chart was developed by research firm Gartner, Inc., and is known as the Gartner Hype Cycle. It's intended as a tool to help investors and business executives assess where an emerging technology stands so they can determine when the time is right to jump in. It helps to think of this phase - where the Bitcoin market currently finds itself - in terms of other technologies that now fall on the right side of the chart.

It helps to think of this phase - where the Bitcoin market currently finds itself - in terms of other technologies that now fall on the right side of the chart. J. Scott Applewhite/AP WASHINGTON -- The U.S. government ran a monthly budget surplus in June, putting it on course to record the lowest annual deficit since 2008. The Treasury Department said Friday that its June surplus totaled $71 billion, following a $130 billion deficit in May. The government also ran a surplus in June 2013, bolstered by dividends from Fannie Mae, the mortgage giant under federal conservatorship for the past six years. For the first nine months of this budget year, the deficit totals $366 billion, down 28 percent from the same period in 2013. Tax receipts are up 8 percent compared to the prior year-to-date, while spending has increased 1 percent. The Congressional Budget Office is forecasting a deficit of $492 billion for the full budget year ending Sept. 30. That would be the narrowest gap since 2008. In 2008, the government recorded a deficit of $458.6 billion, which was the record high for deficits up to that time. But with the outbreak of the recession, deficits soared to unprecedented levels, exceeding $1 trillion for four consecutive years. Tax revenues fell during that period, while government boosted spending in an attempt to stabilize the financial system and provide relief to people who had lost jobs. The yearly deficit peaked at $1.4 trillion in 2009 during the worst of the financial crisis. It gradually fell from there, plunging to $680.2 billion last year. Over the next decade, CBO is projecting that the deficits will total $7.6 trillion. The deficit will fall to $469 billion in 2015 before rising again and topping $1 trillion annually starting in 2023, according to the CBO. Spending on the government's major benefit programs, including Social Security and Medicare, will drive those increases as more baby boomers retire. Republicans have accused President Barack Obama of failing to propose significant cost cuts to reduce soaring entitlement costs. Democrats counter that Republicans would rather impose sharp cuts on needed government programs than impose higher taxes on the wealthy. Neither side is expected to make major concessions in this congressional election year. But the budget wars of the past three years have subsided at least for a brief time. An agreement was reached in December on the broad outlines for spending over the next two years. The agreement will allow Washington to avoid the gridlock that culminated in October's 16-day partial shutdown of the government. The budget cease-fire also includes legislation that will suspend the government's borrowing limit through March 15 of next year. That puts off another battle over raising the debt ceiling until a new Congress takes office in January.

J. Scott Applewhite/AP WASHINGTON -- The U.S. government ran a monthly budget surplus in June, putting it on course to record the lowest annual deficit since 2008. The Treasury Department said Friday that its June surplus totaled $71 billion, following a $130 billion deficit in May. The government also ran a surplus in June 2013, bolstered by dividends from Fannie Mae, the mortgage giant under federal conservatorship for the past six years. For the first nine months of this budget year, the deficit totals $366 billion, down 28 percent from the same period in 2013. Tax receipts are up 8 percent compared to the prior year-to-date, while spending has increased 1 percent. The Congressional Budget Office is forecasting a deficit of $492 billion for the full budget year ending Sept. 30. That would be the narrowest gap since 2008. In 2008, the government recorded a deficit of $458.6 billion, which was the record high for deficits up to that time. But with the outbreak of the recession, deficits soared to unprecedented levels, exceeding $1 trillion for four consecutive years. Tax revenues fell during that period, while government boosted spending in an attempt to stabilize the financial system and provide relief to people who had lost jobs. The yearly deficit peaked at $1.4 trillion in 2009 during the worst of the financial crisis. It gradually fell from there, plunging to $680.2 billion last year. Over the next decade, CBO is projecting that the deficits will total $7.6 trillion. The deficit will fall to $469 billion in 2015 before rising again and topping $1 trillion annually starting in 2023, according to the CBO. Spending on the government's major benefit programs, including Social Security and Medicare, will drive those increases as more baby boomers retire. Republicans have accused President Barack Obama of failing to propose significant cost cuts to reduce soaring entitlement costs. Democrats counter that Republicans would rather impose sharp cuts on needed government programs than impose higher taxes on the wealthy. Neither side is expected to make major concessions in this congressional election year. But the budget wars of the past three years have subsided at least for a brief time. An agreement was reached in December on the broad outlines for spending over the next two years. The agreement will allow Washington to avoid the gridlock that culminated in October's 16-day partial shutdown of the government. The budget cease-fire also includes legislation that will suspend the government's borrowing limit through March 15 of next year. That puts off another battle over raising the debt ceiling until a new Congress takes office in January.

Last but not least, Acasti Pharma is up an impressive 14.5% today. That's not the compelling aspect of this stock right now, however. What makes ACST worth a second look here is that fact that this is the second bullish thrust we've seen from the stock in the past three weeks, with this one being on very high volume. The bulls aren't going away. Indeed, it almost looks like they've been launched out of a slingshot, using some key moving averages as the springboard.

Last but not least, Acasti Pharma is up an impressive 14.5% today. That's not the compelling aspect of this stock right now, however. What makes ACST worth a second look here is that fact that this is the second bullish thrust we've seen from the stock in the past three weeks, with this one being on very high volume. The bulls aren't going away. Indeed, it almost looks like they've been launched out of a slingshot, using some key moving averages as the springboard.